Trump's Return

A counter-revolution that could change everything

First and foremost, expect the launch this week of my new book Breaking Totalitarianism, which will be free as an e-book and provide lots of material on who, how, and why 21st-century totalitarianism is forming in open sight.

In this bulletin, however, I focus on the results of both the US and Irish elections.

This bulletin provides some interpretation of two very different political shifts, one a counter-revolution, the other in a holding pattern.

By some stretch, what is unfolding in the USA will have a much bigger impact on Ireland than anything that has happened last weekend.

Let’s begin with the USA looking at it, through the din, from a sociological and economic perspective.

Trump is Back

The general neurosis has passed through the commentariat like a dose of Epsom salts.

Trump is back.

But is his inbound administration another temporary blip on the road to progressive left liberalism or the swing of the pendulum back to the centre, marking a long-term shift in the Overton Window (the range of policies acceptable to the public as neither extreme nor irrational)?

In reality, both Europe and the USA have shifted the window back from the left towards the centre, in my opinion.

Moreover, the policy platform emerging for the USA will quickly be adapted in Europe, where the phenomenon is apparent from the year of the European elections in Germany, France, Italy, Holland, Austria, Sweden, and Finland.

The hammering the Greens got in Ireland over the weekend is a function of people waking up to the nonsense of net zero and is mirrored in the European elections and by the Republicans in the USA.

America's Economic Resilience Defies Skeptics

Despite the doomsayer industry of talk show panellists, videos, podcasts, and books, the US Treasury market has so far stood up, and with it the US electoral system.

Trump’s Republicans have taken all three houses: the White House, Congress, and the Senate.

It is a clear mandate for the reform policy program and a clear rejection of the Democrat platform of business as usual.

In practice, Trump’s platform is, for all intents and purposes, counterrevolutionary.

He is squarely going after the Deep State and its forever wars, which means an attempt to dismantle its vast tentacles across key aspects not just of government business in the military defence complex, foreign policy, and the oligarchy interface but also in pharma captivity of regulators and the capture of US media itself.

Elon Musk is tasked with leading DOGE, to chop into government waste; there’s plenty of that, likely to amount to trillions by the time he is done lightening the US deficit.

Meanwhile, Robert F. Kennedy Jr., a favoured target of the Left (and whose works I’ve studied, as you know), is going after the pharma-processed food complex in an attempt to address the huge rates of chronic disease in the USA.

In a blizzard of announcements, Trump is talking tough on tariffs against importers. This is lost in a media sworn to present the developer as a vengeful dictator.

However, Trump’s behaviour is nothing new.

These stances marked his first presidency and are opening negotiating positions. Trump is being Trump, mouthy and staking out his opening position, but, in reality, his compromise will be different, especially with Europe once cycled through the washing machine of economics, international politics, and geopolitical reality.

Press hard on Europe, and the USA knows full well that an isolationist US will fast-forward what it most fears, the development of a Eurasian economic block running from the Aran Islands to the Pacific and centred on Paris, Rome, Berlin, and Moscow, where Western Europe comes with the wealth and know-how and Russia with the energy and natural resources.

The USA remains the standout economic powerhouse, built on a virtuous circle of assets: deep capital markets, robust institutions, a growing population, huge military power, and the world reserve currency in the US dollar.

As a colossus, it faces serious challenges; the debt to GDP is eye-watering, raising concerns about its capacity to access credit at affordable prices, much of its infrastructure is old, and its people are grumpy and divided along key lines.

These are big problems but not insurmountable.

The USA will prolong its run as the world’s leading economy and ownership of the world reserve currency for a while yet, mostly because there isn’t an alternative.

Communist China, with its capital controls and ruthless surveillance of its fast-ageing population, is grappling with a massive property and debt overhang and is not capable of providing anything more than regional leadership.

Fatalities in its armed forces would end huge numbers of Chinese bloodlines due to the legacy of its one-child policy, and now, as a consumer economy, it no longer enjoys the cheapest labour status; that has passed to regional rivals.

The BRICS attempt to create a dollar alternative is not only challenged by the complexity of pressing together diverse, dispersed economies on different economic cycles but also now faces Trump’s promise to block US market access for doing so.

Europe remains sclerotic, ageing, stifled by regulation, and unsure of itself, its existential risk worsened by outsourcing security to the US-led NATO, which many analysts think would last but a few days in a conventional war with Russia.

Neither favour such a disastrous confrontation (see Draghi’s Report Card on Europe below).

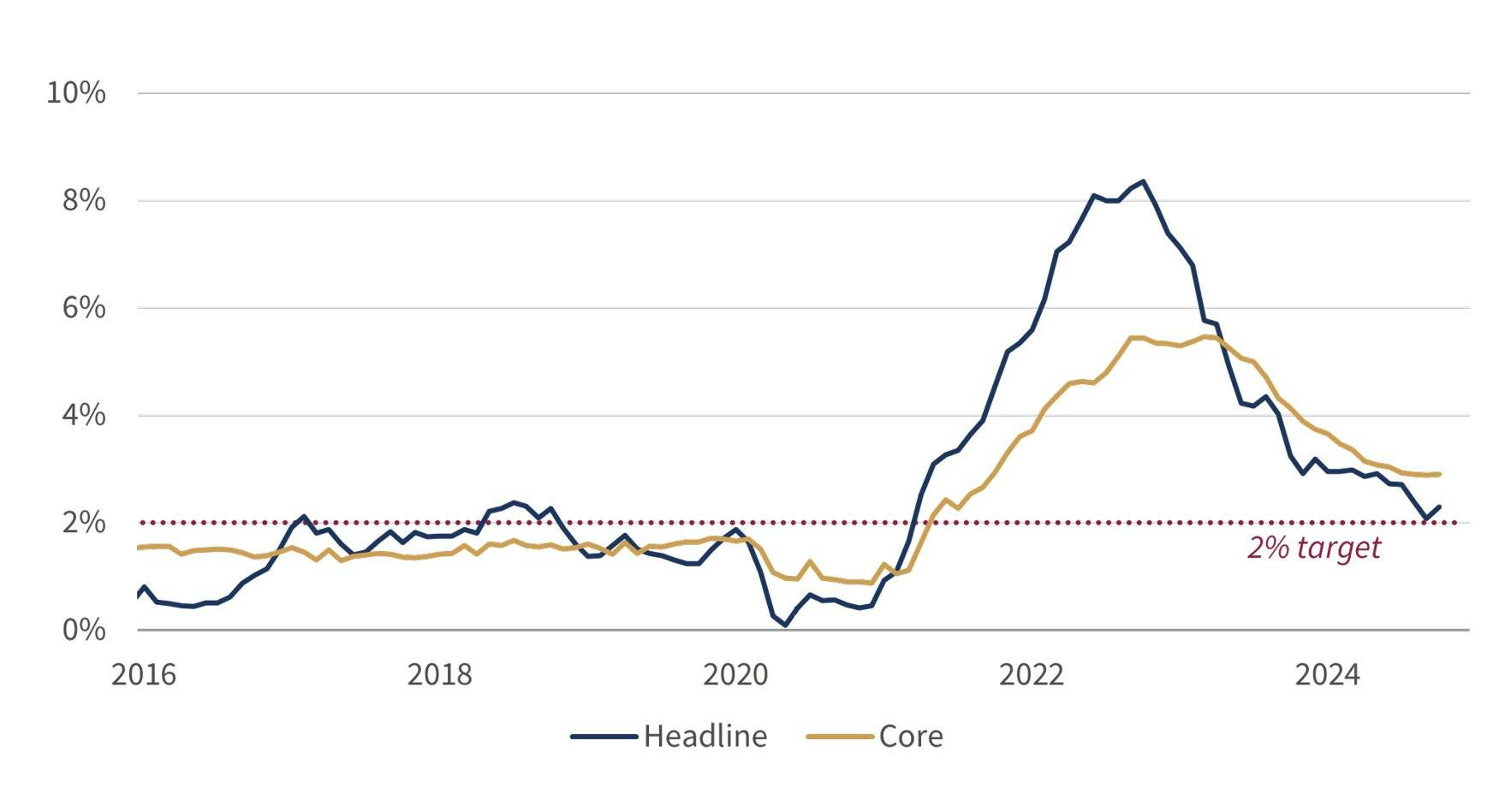

USA and the rest of the developed world have emerged from a horrible period of nose-bleeding rate hikes, up fivefold from 2021.

This followed two years of intermittent lockdowns and widespread closures and losses of business that would normally mean we ought to be in deflation or depression. Instead, we were dished up excess inflation of at least 20%, reducing the purchasing power of money drastically in a short window.

Inflation has been tempered, running at 2.9% in the USA and 1.8% in the Eurozone from heights touching on double digits.

The rate-cutting cycle has begun, albeit slowly, but US futures markets still flash another 2% rate cut over the next two years (for readers who invest in financial assets, that translates into a continued bounce back in bond funds and supports equities through cheaper credit).

Patience is needed before this extraordinary hiking and cutting cycle enters the history books.

But, if you look beneath the billion-dollar mud-throwing melee that passes for a US presidential election these days, and what do you see?

Signs of improved risk-taking favouring equities.

A job-producing engine, with 1.2 vacancies per unemployed.

Household purchasing power is up 4.4% as 2024 closes out.

Fast tech adoption, ChatGPT is already past 100 million users.

More liquidity as rates cut supportive of cheaper long-term mortgage debt.

Surging stock market led by tech giants after breaking out of the COVID drift.

The Age of Productivity and Improved Living Standards?

“Productivity isn't everything, but, in the long run, it is almost everything. A country's ability to improve its standard of living over time depends almost entirely on its ability to raise its output per worker."

Paul Krugman (The Age of Diminished Expectations, 1990).

Look over the immediate horizon, and the growing muscle mass for a long-term economic cycle is apparent.

Notwithstanding the social challenges all this change brings, such as workforce replacement with technologies, the net result is higher productivity and economic expansion.

There is a shift to a multipolar world order.

The health industry must respond to the ageing of the West.

The energy transition affecting all countries will not be smooth.

There is very fast-moving technological change across many vectors, not least in quantum computing.

After the discombobulation, we may not feel like welcoming the new guest, but it is here: the 4th Industrial Revolution has arrived and will stay for decades if we can, collectively, avoid catastrophe from geopolitical failures and rising 21st-century totalitarianism.

In that regard, the US counter-revolution, for that’s what it is, promises to offload virtue signalling woke policies:

Critical Theory

Queer Theory

Climate Alarmism (or what Trump calls the Climate Scam)

This is all part of a Trump-led attack on the stranglehold of the Deep State and much leaner government, betting that resurgent economic power will not throw the debt out of whack and unity may be restored in time by real gains for workers and the US middle classes.

It is a huge task.

The journey will be very bumpy, but it has begun.

Entering into the foot of this era, Trump’s economic policy platform advocates for tax cuts and a war on red tape.

The gambit is that over time this will surge US GDP and lessen the debt burden per dollar created but at the risk of higher inflation and pushing up US bond yields as credit markets price in the risk.

This is already happening.

After hitting a low of 3.6% in mid-September in anticipation of the first of the FED cuts, the key US 10-year bond yield climbed to 4.47% by mid-November only to retreat by month-end to 4.22%.

For the first time in modern history, the bond curve will be impacted by the work of a waste tsar and oligarch, Elon Musk.

If he succeeds, which will be quickly seen, the impact on Europe will be profound—the pendulum may swing towards slimmer government and conservative policies.

Trump's Policies at a Glance: A Sweeping Vision for Economic Change

Slash corporate tax by 6% to 15% and reinstate unlimited state and local tax deductions.

Deport much of the USA’s 11 million illegal immigrants, some 4% of the labour force, using catch and release policies.

Increase tariffs on Chinese goods to 60% and ban ownership of critical infrastructure.

Settle the Russia-Ukrainian War and reform NATO, enforcing increased spending by members.

Cut costs of drugs, increase competition, slim down red tape with focus on improved US health.

Repeal Biden’s climate policies and encourage fossil fuel drilling and mining key minerals.

Shrivel excess red tape with a special focus on energy, construction, and finance.

Draghi’s Report Card on Europe

The former European Central Bank chief’s recent report won’t come as a surprise to Europe watchers. He nails down the challenges faced.

A virtuous circle of interconnections evolves over a long time such as those experienced in the USA and in economies like Switzerland.

These have cultural, attitudinal, financial, and philosophical inputs not merely related to finance and institutions.

It is why Americans think differently and why they see failure as a learning and development opportunity and not a means to demean and dismiss risk takers.

Draghi identifies the productivity and innovation gap between Europe and the US, pointing to the technology sector, which means the USA will scale faster and stay in front given its huge investment in R&D.

There is a shortage of EU venture finance, he finds, and, overall, much lower risk-taking relative to savings in banks and in bonds.

He also identifies fragmentation in markets, variable governance standards, and a skills shortage in mathematics, science, technology, and engineering.

Especially obvious is Europe’s poor energy security, high energy costs, and poor access to critical raw materials.

No marks for the emphasis on excessive regulation and bureaucracy. Ever tried opening a bank account?

As a banker, Draghi naturally proposes the issuance of EU bonds to deepen capital markets and so assist in growing innovative enterprises; overall investment spending needs to ramp up 4%-5% of GDP annually.

Look through the economic language, and the scorecard is a clarion call for revolutionary reform within the EU and Eurozone, or face stagnation.

Irish General Election: Old Institutions Crumble as Reality Bites

Firstly, bear in mind that in these tectonic movements on both sides of the Atlantic, the Dáil, as demonstrated by voting for the EU Migration Pact, by pushing queer theory into kids classrooms, and by attempting to redefine marriage in the roundly rejected constitutional referendum, hardly matters.

The Dáil will follow, not lead.

So much Irish sovereignty has been ceded to the EU for so long, together with ceding to supranational organisations like the WHO and UN, joined at the hip to the WEF and its stakeholder capitalism, that both the political and civil service establishment have become captive.

It is noteworthy that not a single politician of any note focused this dynamic on the diminution of the Dáil or used the behaviour around the false pandemic as evidence.

This week I will launch, free as an e-book, Breaking Totalitarianism to awaken more Irish readers to what is really happening, why, and by whom, using what processes. More information to follow very soon.

In the meantime, my analysis on the general election:

The crushing of the Greens is consistent with public shifts in the USA and Europe against the zero-carbon woke narrative and against the nonsense of so-called consensus science, which is a political ideology, not science.

The fear mongers are losing their grip the longer the fantastic illusion of their spectacular science ages and the more proper science and the upside-down economics of zero carbon break through to real-life experiences, such as selling a used EV.

There is a direct line to rampant housing and rental prices and the Cead Mile Failte that the virtue-signalling Green leader promulgated abroad.

Their wipeout as a political force is irreversible as the world shifts away from getting poorer to getting more prosperous, from fear to hope.

Europe itself has a massive hangover from failed green policies in Germany, whose economy is in decline while the rest of Europe watches aghast.

Sinn Féin is outed as a transfer-toxic, unfit, and untrustworthy main opposition party, leading to growth for Labour and Social Democrats.

Cut through the SF spin, and it has lost ground since 2020.

It has no route to government in the present calculus because its leadership managed to blow poll support, which has nearly halved based on these results.

There is no Shinner Dawn.

The vote management performance of Fianna Fáil is very much old school and a commendable performance.

But overall, the uni-party space is thinning when Fine Gael is added. Their support at the edge is promiscuous, largely due to a change in tone (not policy) on fake refugees after Varadkar exited and the revenue largesse constructed on bumper Corporation Tax receipts arrived in a Late Late type budget.

Atomised, the Independent sector did not surge.

The Fine Gael narrative shift took away its single-issue oxygen, exposing political inexperience. The failure to reach a common accord, even a single policy, is a brutal lesson in politics.

The Hutch surge was an act of contempt, a Councillor Bernard Murphy moment, best noted, then forgotten.

Conclusion

The new US administration is geared up to robustly reform the US economy and is not some ogre let loose to bully nation-states in the fashion of the exploitative era of buccaneering mercantilists.

Despite the shift towards a multipolar world, prosperity depends on mutual trade hammered out in trade negotiations that fail unless both sides gain.

Trump and his aides know how the game goes.

The dramatic emphasis on thinner government comes not a moment too soon to alter the direction of the US debt-to-GDP trajectory. It is Musk’s singular focus, without which the Colossus would inevitably unravel.

How long Trump’s enormous ego suffers Musk’s remains a concern.

Events in the USA may be good for Europe, alarmed by Draghi’s scorecard and the degree to which Europe is falling behind and defensively is vulnerable militarily and in terms of energy security.

Europe’s relative growth is impeded by its outsized bureaucracy, which reaches deep into the professions, finance, planning, etc.

Unadjusted Europe will continue to fall behind, but a peaceful outcome to the Ukrainian-Russian war ought to quickly reopen energy supply lines, short of which it is hard to see how Germany doesn’t continue to decline.

If geopolitical risks can be calmed by Trump, who professes to be anti-war, a strong growth period lies ahead.

For those investing in financial assets favouring US risk assets, Asia post a new Sino-American trade deal is the way to think things through.

Europe can get cheaper, but without a strategy for reform, there will be good reason for why it is cheap.

Gold ought to continue its run up, albeit after a recalibration reflecting concerns about global debt excesses and marking a weakening US dollar.

Kind regards,

Eddie